If your employer offers health insurance benefits, one of your options may be a high-deductible health plan (HDHP) with eligibility for a health savings account (HSA). These plans offer potential savings by encouraging you to make cost-effective choices in your medical spending. If you do not have employer-sponsored health coverage, you can choose from a variety of individual HDHPs, including plans through state or federal health insurance exchanges.

Lower Premiums, Higher Deductibles

Premiums for HDHP coverage are generally lower than for traditional preferred provider organization (PPO) coverage. In exchange, you pay a larger annual deductible before the plan begins to cover a percentage of expenses.

Certain types of preventive care, such as annual physicals, health screenings, and selected medications, may be covered without a deductible (in some cases, provided at no cost). HDHPs can also offer telehealth and other remote health-care services without a deductible through 2024. Regardless of the deductible, the costs for medical services may bereduced through the insurer's negotiated rate.

To protect consumers from catastrophic expenses, most health insurance plans have an annual out-of-pocket maximum above which the insurer pays all medical expenses. HDHP maximums are generally higher than those of traditional plans. But if you reach the annual maximum, your total cost for that year would typically be lower for an HDHP, with the up-front savings on premiums. If you have low medical costs, the lower premiums also will generally make an HDHP more cost-effective. For other scenarios, the cost-effectiveness of an HDHP may vary with your situation. Although an HDHP might save money over the course of a year, some consumers could be hesitant to obtain appropriate care because of the higher out-of-pocket expense at the time of service.

Triple Tax Advantage

You must be enrolled in an HDHP to establish and contribute to an HSA, which allows investments within the account and offers three powerful tax advantages: (1) contributions are deducted from your adjusted

gross income, (2) investment earnings compound tax-free inside the HSA, and (3) withdrawals are tax-free if the money is spent on qualified medical expenses (including dental and vision expenses). Some states do not follow federal tax rules on HSAs.

HSA contributions are typically made through payroll deductions, but in most cases, they can also be made directly to the HSA provider. In 2023, contribution limits are $3,850 for an individual and $7,750 for a family ($4,150/$8,300 in 2024), plus an additional $1,000 if the account holder is age 55 or older. Although 2023 payroll contributions must be made by December 31, you can make direct contributions for 2023 up to the April 2024 tax deadline. Some employers contribute to an employee's HSA, and any employer contributions would be considered in the annual contribution limit.

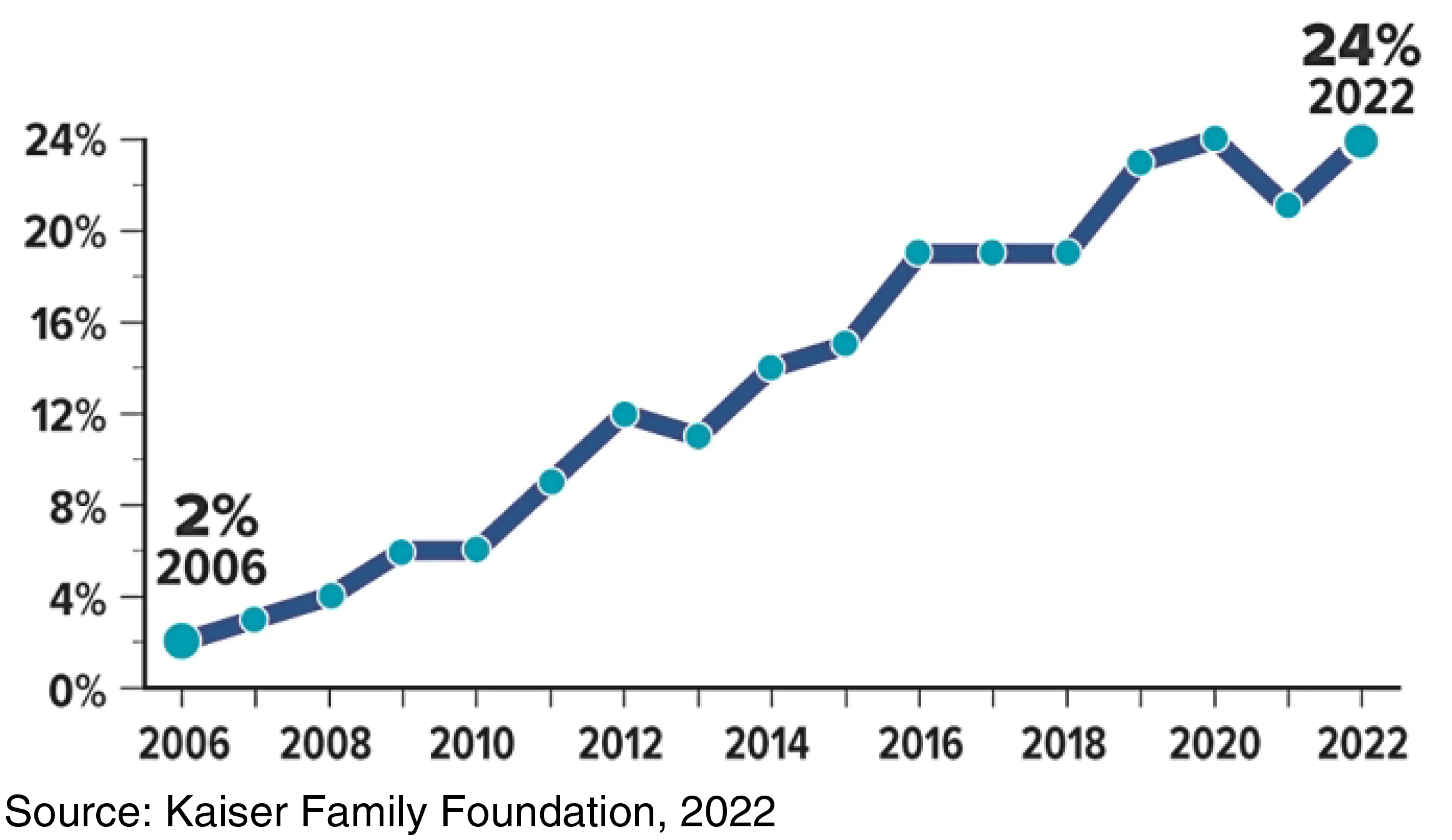

Growing Trend

Percentage of covered workers enrolled in an HSA-eligible high-deductible health plan

Saving for the Long Run

Many people use HSAs to pay health-care expenses as they go, but there are advantages to paying from other funds and allowing the HSA to accumulate and pursue tax-deferred growth over time. Assets in an HSA belong to the contributor, so they can be retained in the account or rolled over to a new HSA if you change employers or retire. Unspent HSA balances can be used to help meet health-care needs in future years whether or not you are enrolled in an HDHP; however, you must be enrolled in an HDHP to contribute to an HSA.

Although HSA funds cannot be used to pay regular health insurance premiums, they can be used to pay Medicare premiums and long-term care costs, which could make an HSA an excellent vehicle to help fund retirement expenses. After you enroll in Medicare, you can no longer contribute to an HSA (because Medicare is not an HDHP), but you can continue to use the HSA funds tax-free for qualified expenses. After age 65, you can withdraw HSA funds for any purpose without paying the 20% penalty that typically applies to those under age 65, but you would pay ordinary income taxes, similar to a withdrawal from a traditional IRA. All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy will be successful.

IMPORTANT DISCLOSURES

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Advisory services offered through Buska Wealth Management, LLC an SEC Investment Advisor. Insurance products and services are offered through Buska Retirement Solutions, Inc., an affiliated company. Buska Wealth Management, LLC's outgoing and incoming emails are electronically archived and subject to review and/or disclosure to someone other than the recipient. We cannot accept requests for securities transactions or other similar instructions through email. We cannot ensure the security of information e-mailed over the Internet, so you should be careful when transmitting confidential information such as account numbers and security holdings. If the reader of this message is not the intended recipient, or an employee or agent responsible for delivering this message to the intended recipient, you are hereby notified that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please notify us immediately by replying to this message and deleting it from your computer.