Life insurance can serve many valuable purposes. However, later in life — when your children have grown, you've retired, or you've paid off your mortgage — you may think you no longer need to keep your coverage, or perhaps your coverage has become too expensive. You might be tempted to abandon the policy or surrender your life insurance coverage, but there are other alternatives to consider.

Term vs. Perm

If you have term life insurance, you generally will receive nothing if you surrender the policy or let it lapse by not paying the premiums. However, depending on your age, your health status, and the time left in the term, you may be able to extend the coverage or convert the policy to a permanent policy. The rules for extension and conversion vary by policy and company.

On the other hand, if you own permanent life insurance, the policy may have a cash surrender value (CSV), which you can receive upon surrendering the insurance. If you surrender your cash value life insurance policy, any gain resulting from the surrender (generally, the excess of your CSV over the cumulative amount of premiums paid) will be subject to federal and possibly state income tax. Also, surrendering your policy prematurely may result in surrender charges, which can reduce your CSV.

Exchange the Old Policy

Another option is to exchange your existing permanent life insurance policy for either a new life insurance policy or another type of insurance product. Under the federal tax code, this is known as an IRC Section 1035 exchange.

The exchange must be made directly between the insurance company that issued the old policy and the company issuing the new policy or contract. The rules governing 1035 exchanges are complex, and you may incur surrender charges from your current life insurance policy. In addition, you may be subject to new sales, mortality, expense, and surrender charges for the new policy.

Here are some options for a 1035 exchange.

Lower the premium. If the premium cost of your current life insurance policy is an issue, you may be able to lower the premium by reducing the death benefit, which would not require an exchange. Or you can try to exchange your current policy for a policy with a lower premium cost. However, it's possible that you may not qualify for a new policy because of your age, health problems, or other reasons.

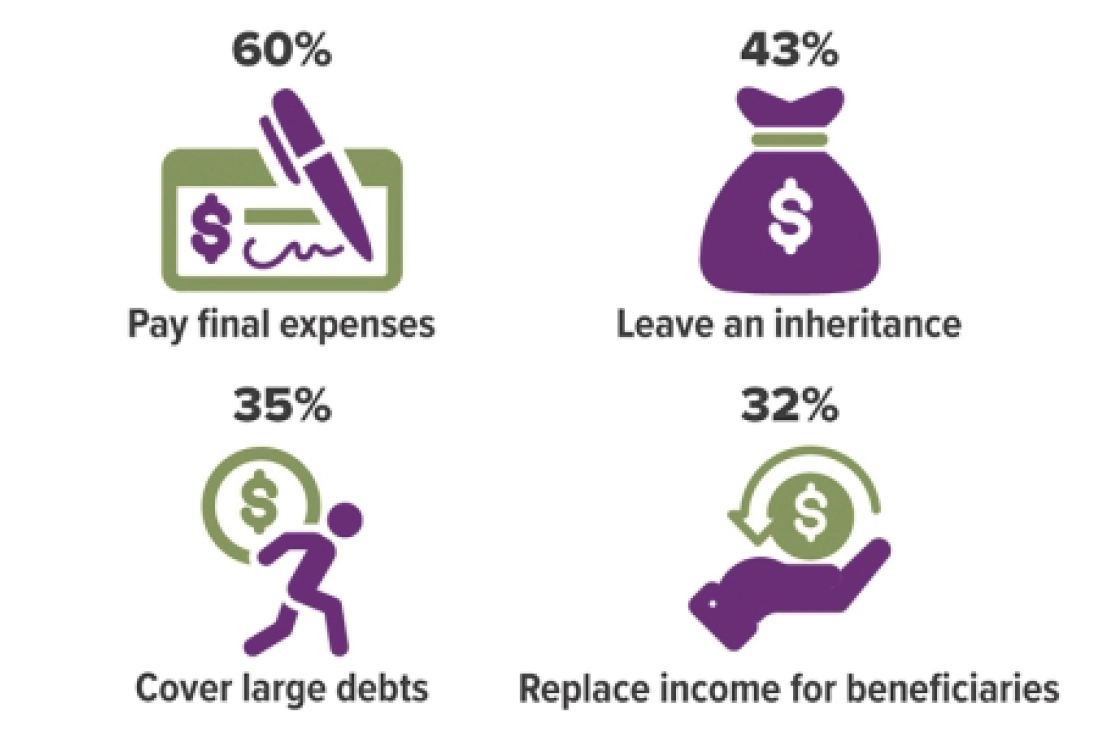

Why Buy Life Insurance?

Although life insurance has traditionally been viewed as a way to replace income after the death of a wage earner, consumers are more likely to give other reasons for purchasing coverage.

Create an income stream. You may be able to exchange the CSV of a permanent life insurance policy for an immediate annuity, which can provide a stream of income for a specific period of time or for the rest of your life. Each annuity payment will be apportioned between taxable gain and nontaxable return of capital. You should be aware that by exchanging the CSV for an annuity, you will be giving up the death benefit, and annuity contracts generally have fees and expenses, limitations, exclusions, and termination provisions. Also, any annuity guarantees are contingent on the financial strength and claims-paying ability of the issuing insurance company.

Provide for long-term care. Another option is to exchange your life insurance policy for a tax-qualified long-term care insurance (LTCI) policy. Any taxable gain in the CSV is deferred in the long-term care policy, and benefits paid from the tax-qualified LTCI policy are received tax-free. Keep in mind that if an LTCI policy does not accept lump-sum premium payments, you would have to make several partial exchanges from the CSV of your existing life insurance policy to the LTCI policy provider to cover the annual premium cost. A complete statement of coverage, including exclusions, exceptions, and limitations, is found only in the policy. Carriers have the discretion to raise their rates and remove their products from the marketplace.

Whatever option you choose, it may be wise to leverage any cash value in your unwanted life insurance policy to meet other financial needs.

IMPORTANT DISCLOSURES

Broadridge Investor Communication Solutions, Inc. does not provide investment, tax, legal, or retirement advice or recommendations. The information presented here is not specific to any individual's personal circumstances.

To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable — we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

Wealth Management, LLC an SEC Investment Advisor. Insurance products and services are offered through Buska Retirement Solutions, Inc., an affiliated company. Buska Wealth Management, LLC's outgoing and incoming emails are electronically archived and subject to review and/or disclosure to someone other than the recipient. We cannot accept requests for securities transactions or other similar instructions through email. We cannot ensure the security of information e-mailed over the Internet, so you should be careful when transmitting confidential information such as account numbers and security holdings. If the reader of this message is not the intended recipient, or an employee or agent responsible for delivering this message to the intended recipient, you are hereby notified that any dissemination, distribution, or copying of this communication is strictly prohibited. If you have received this communication in error, please notify us immediately by replying to this message and deleting it from your computer.